Important note

1. Information relating to the five most important execution venues

2. Participation policy

1. Information relating to the five most important execution venues

(pursuant to Annex II, Table 1 Delegated Regulation (EU) 2017/576)

Bad Homburg, in Dezember 2023

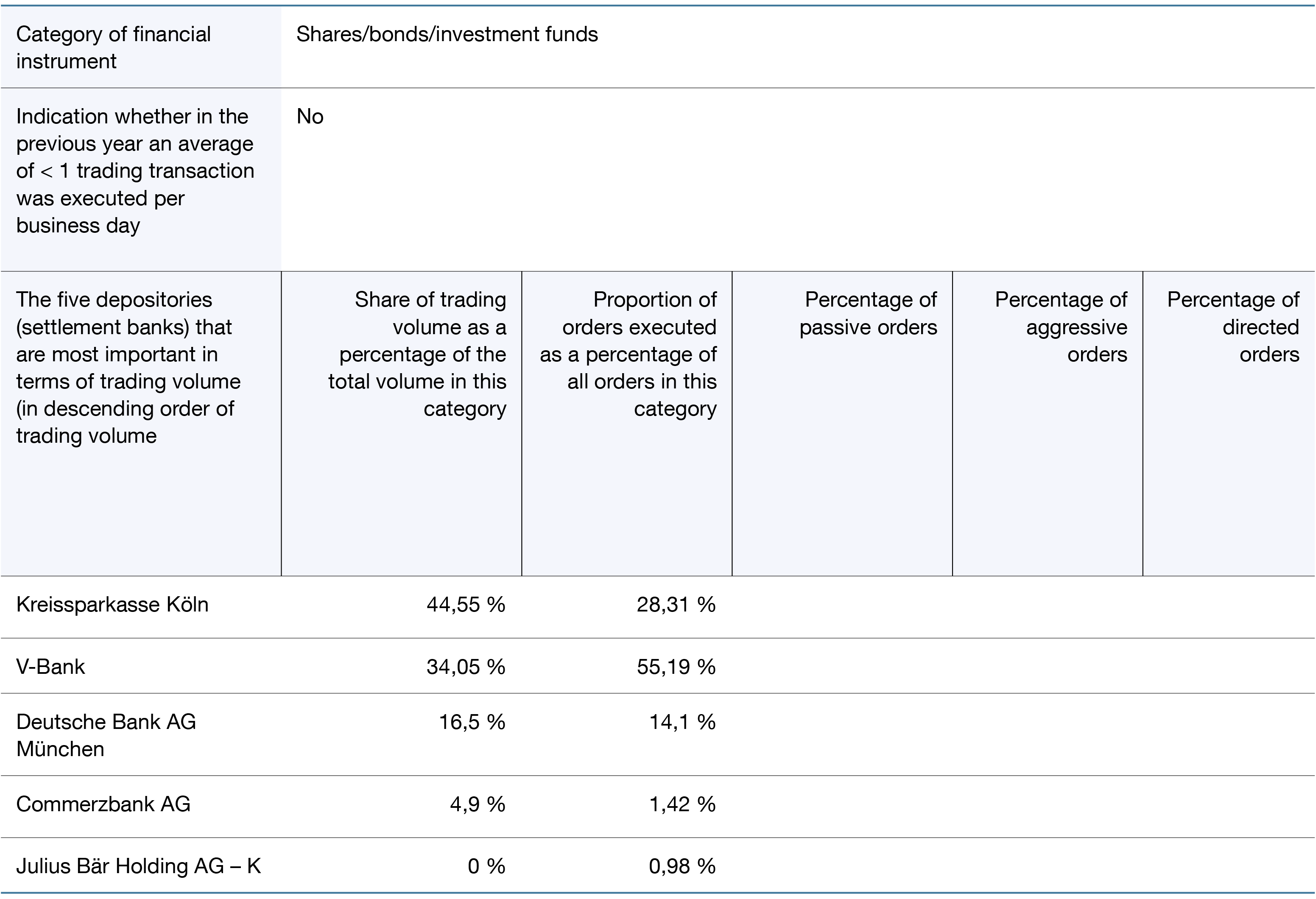

A new feature of MiFID II is the obligation of the institute, to annually publish the five execution venues for each category of financial instrument on its website, which are most significant in terms of trading volumes through which it executed client orders in the previous year, and to summarise information on the quality of execution achieved (Section 82, Sub-section 9 Securities Trading Act). As the institute selected other investment firms for transacting client business, the five most important custodian depots (settlement banks) are to be named in this case and information on these firms regarding the quality of execution achieved summarised. Further information on this publication can be found in the Delegated Regulation (EU) 2017/576. According to ESMA, the reports are to be made available on the website for at least two years.

Note: The data refers to the business year (1 January to 31 December 2023) of the institute.

Summary of the execution quality (“quality record”) achieved for the year 2020 (pursuant to Article 3 (3) Delegated Regulation (EU) 2017/576)

A) Relative significance of the execution factors

As a matter of principle, HQ Trust GmbH does not pass investment decisions directly to trading centres, rather to the client’s respective depot bank, which executes the instructions. Though careful selection and monitoring of the banks, HQ Trust GmbH works towards the best possible implementation of the trading decisions.

In the context of wealth management, we are obliged by Article 65 of the Delegated Regulation 2017/565 to act in the best interests of our clients and take all adequate measures to achieve the best possible results for our clients. In order to comply with these stipulations, we select the executing institutions so that their execution principles ensure the best possible order implementation, in particular that the best possible result is achieved for our clients.

Our selection criteria are:

- Pricing of financial instruments (purchase price and sales price)

- Overall costs of the order processing

- Speed of order processing

- Likelihood of order implementation

- Practicability of electronic transaction platforms

These criteria are to be weighted taking customer order, the financial instrument and the place of execution into consideration.

During the course of the business relationship, we monitor whether the executing institutions carry out the orders in compliance with their executions principles. Once a year, we verify the execution policies of the executing institutions for compliance with the above criteria and, where appropriate, would amend the selection.

B) Associations, conflicts of interest and joint ownerships relating to banks or execution venues

There are no close connections, conflicts of interest or joint ownerships relating to banks or execution venues.

C) Special agreements with banks or execution venues relating to payments made or received or discounts, trade allowances or other non-monetary considerations received

No special agreements apply with banks or execution venues with regard to payments made or received or discounts, trade allowances or other non-monetary considerations received.

D) Addition, removal or replacement of banks or execution venues

No changes of the selected banks were undertaken in the wealth management portfolio.

E) Explanation regarding execution decisions, where the portfolio manager treats different client categories differently

HQ Trust does not differentiate in the execution between private clients and professional clients.

F) Explanation where, in the execution of trading decisions for the account of private clients, criteria other than rates were given precedence

The best possible results are based on the complete price, made up of the price for the financial instrument and all other costs associated with the execution of the order (including fees and charges levied by the place of execution, costs for clearing and processing and all other charges).

G) Explanation regarding the use of any data or tools in the context of the quality of execution, including data published by the trading centres pursuant to RTS 27

During the course of the business relationship we monitor whether the executing institutions carry out the orders in compliance with their execution policies. This ensues on the basis of the confirmation of execution or bought/sold notes which we receive from the executing institutions.

H) Explanation where the information of consolidated tape providers (CPA) is used

No consolidated tape provider is used.

2. Participation policy

Description and publication of the participation policy of HQ Trust GmbH pursuant to Section 134b of the German Stock Corporation Act (AktG)

HQ Trust GmbH - hereinafter referred to as the "Institute" - as an asset manager within the meaning of Section 134a (1) No. 2 of the German Stock Corporation Act (AktG) is subject to the provisions of Sections 134b and 134c of the German Stock Corporation Act (AktG) and must therefore describe and publish its participation policy within the meaning of Section 134b (1) of the German Stock Corporation Act (AktG).

The Institute does not exercise any shareholder rights on behalf of its customers. No shareholders' meetings are attended, no voting rights are exercised on behalf of customers, notifications from stock corporations are only acknowledged within the scope of mandatory notifications, and no active communication takes place with the Company or with other shareholders.

Therefore, the participation policy has been established as follows:

-

the Institute does not exercise any shareholder rights within the meaning of Section 134b (1) no. 1 of the German Stock Corporation Act (AktG) that are based on participation in the Company. In particular, it does not exercise any rights related to general meetings of stock corporations. The right to a share in profits within the meaning of sections 60 et seq. AktG (German Stock Corporation Act) as well as to subscription rights are exercised in consultation with the customers.

-

the monitoring of important matters of the companies within the meaning of Section 134b (1) No. 2 of the German Stock Corporation Act (AktG) is carried out by taking note of the legally required reporting of the companies in financial reports as well as ad hoc announcements.

-

there shall be no exchange of views with corporate bodies and/or stakeholders of the Company within the meaning of Section 134b (1) no. 3 AktG.

-

there shall be no cooperation with other shareholders within the meaning of section 134b (1) no. 4 of the AktG.

-

in the event of conflicts of interest within the meaning of section 134b (1) no. 5 AktG, these shall be disclosed to the parties concerned in accordance with the statutory provisions and the further course of action shall be clarified with the parties concerned.

-

annual reporting on the implementation of the participation policy within the meaning of Section 134b (2) of the German Stock Corporation Act (AktG) is not carried out, as no corresponding rights are exercised.

Voting behavior within the meaning of Section 134b (3) AktG is not published, as no participation in voting takes place.